{kind=link}

Understanding the price of a million-dollar life insurance coverage coverage may be pivotal in securing your loved ones’s monetary future. However have you ever ever puzzled simply how accessible or pricey such a coverage is likely to be?

Do you assume a million-dollar time period life insurance coverage coverage appears like an excessive amount of insurance coverage?

As a Licensed Monetary Planner,I see underinsured individuals on daily basis.

What do I inform them?

One million-dollar time period life insurance coverage coverage may truly be the minimal protection wanted for the everyday middle-class family,nevertheless it’s reasonably priced.

That may sound like an exaggeration,however should you crunch the numbers – simply as we’ll be doing slightly bit – you’ll understand{that a}million-dollar coverage is likely to be simply what you want.

The excellent news is time period life insurance coverage isn’t almost as pricey as most individuals assume.

What makes time period life insurance coverage even higher is that bigger insurance policies price much less on a per thousand foundation than smaller insurance policies do. You could discover the premium on a $1 million coverage is simply slightly bit greater than it’s for $500,000.

Do You Actually Want a $1 Million Time period Life Insurance coverage Coverage?

In all probability,however let’s discover out. A basic rule of thumb is that you need to get 10x your earnings as baseline protection for all times insurance coverage.

Should you’re younger,which may be low as a result of it’s possible you’ll need to present your loved ones with sufficient to interchange your earnings for 15 years or extra.

Right now,$1 million has turn out to be the brand new baseline for life insurance coverage by a major breadwinner. Something much less might go away your loved ones financially impaired.

Typical Obligations to Add When Calculating the Quantity You Want

Right here’s an inventory of all of the totally different obligations it’s possible you’ll need to have life insurance coverage cowl within the unlucky occasion you cross away early.

- Your Earnings (And for How Many Years)

- Any Debt You Could Wish to Be Settled

- Future Obligations Equivalent to School for Kids

- Different Obligations Equivalent to Enterprise

- Typical Objects You Can Subtract When Calculating the Quantity You Want

- Present Life Insurance coverage Insurance policies

- Belongings (Like Money or Inventory) You May Select to Use As an alternative of Life Insurance coverage

Now that you’ve an thought of those obligations,let’s punch them into this life insurance coverage calculator to search out out should you want a million-dollar coverage.

Selecting A Million Greenback Insurance coverage Coverage

In keeping with CoverageGenius,the typical price for a 20-year $1 million time period life insurance coverage coverage for a 35-year-old male is $53 monthly. Nonetheless,your fee will differ in accordance with the next components.

Components that have an effect on your fee:

- Your Protection Quantity and Coverage Time period

The place to begin?

The perfect,and best place to begin is on-line. I like to recommend having two or three insurers compete for your enterprise to be sure to get the perfect fee and protection. To see how low-cost time period life may be,select your state from the map above to be matched with high life insurance coverage suppliers immediately.

Components That Have an effect on How A lot You Want

Let’s have a look at the person parts that may rapidly add as much as over a million-dollar coverage.

Earnings Alternative

That is the place issues can get a bit intimidating. Even should you earn a modest earnings,it's possible you'll want near $1 million to interchange that earnings after your loss of life to be able to present for your loved ones’s fundamental dwelling bills.

The traditional knowledge within the insurance coverage business is that you need to keep a life insurance coverage coverage equal to between 10 occasions and 20 occasions your annual earnings. So should you earn round $50K per yr,that might imply coverage protection between $500K and $1 million.

The complication right this moment is that with rates of interest being as little as they're that may not be sufficient both.

For instance, you probably have a $1 million coverage that might be invested at 5% per yr, your loved ones might dwell on the curiosity earned – which conveniently involves $50,000 per yr – for the subsequent 20 years.

That will nonetheless go away the unique $1 million intact to cowl different bills. However with right this moment’s microscopic rates of interest, there’s no solution to get a assured return of 5% in your cash, definitely not for 15 or 20 years.

EXPERT TIP

That brings us again to simple arithmetic – multiplying your annual earnings occasions the variety of years your loved ones’s dwelling bills will have to be coated. This alone can require a $1 million life insurance coverage coverage.

Additionally, remember that most insurance coverage firms have a most multiplier you possibly can apply to your earnings for all times insurance coverage protection. For instance, it wouldn’t make a lot sense for a 22-year-old making $27,000 per yr to get a $2 million life insurance coverage. Or a 65-year-old that's retired to safe a $3 million greenback coverage.

The desk beneath is roughly how a lot you’re allowed to multiply your earnings primarily based in your age and earnings:

| Applicant’s Age | Annual Earnings Multiplier |

| 18-29 | 35x |

| 30-39 | 30x |

| 40-49 | 25x |

| 50-59 | 20x |

| 60-69 | 15x |

| 70-79 | 10x |

| 80+ | 5x |

Utilizing the desk above as a information,a 35-year-old making $150,000 per yr can be capped at taking out a $4.5 million time period coverage ($150,000 x 30=$4,500,000).

Your Remaining Bills

Right here we begin with the fundamentals – wrapping up your last affairs.

It will embrace funeral prices and any lingering medical prices. An inexpensive estimate for a typical funeral is round $20,000.

Loopy,proper? You will get burial insurance coverage to cowl solely essentially the most fundamental of ultimate bills.

Excellent Debt

Debt burdens are excessive within the US,and debt may be particularly crushing on remaining relations. Many life insurance coverage prospects be certain they'll repay most of their debt with the coverage.

Medical Debt

Medical prices are a severe variable. Even you probably have glorious medical health insurance, there are prone to be unpaid medical payments lingering after your loss of life. This has to do with copayments, deductibles, and coinsurance provisions.

Collectively, they'll add as much as many 1000's of {dollars}. However the place issues get actually difficult is should you die of a terminal sickness.

For instance, if you're laid low with an sickness that lasts for a number of years,you would incur quite a few bills that aren't coated by insurance coverage. This may occasionally embrace the price of private care and even experimental therapies.

Mortgage

A house could also be a big asset, nevertheless it’s additionally typically a house owner’s largest debt. The common mortgage stability within the US is roughly $236,443 in accordance with Experian knowledge. So you would simply use a life insurance coverage coverage to repay that debt and relieve your family members of a month-to-month mortgage cost.

Private Debt

Bank card debt and different private debt are among the costliest obligations carrying charges upward of 20% in some instances. Ensure you have sufficient to cowl this very costly debt.

Future Obligations For Your Household

Under is a sampling of main bills your loved ones is prone to incur, both on an annual foundation or in some unspecified time in the future after your loss of life.

School

Tuition prices proceed to skyrocket. The Division of Training means that four-year public faculty tuition has been rising a mean of 5% per yr, far exceeding the speed of inflation. If in case you have one youngster who attends an in-state public college, a second at an out-of-state public college, and a 3rd in a personal college, the full expenditure will attain $416,560.

- Annual price at in-state public faculty: $20,770 ($83,080 for 4 years)

- Annual price at out-of-state public faculty: $36,420 ($145,680 for 4 years)

- Annual price at a personal faculty: $46,950 ($187,800 for 4 years)

Transportation

Automobiles and different types of transportation symbolize one other giant sum. Sadly, with rising electronics and security options, the typical price of a brand new automotive continues to develop.

Well being Insurance coverage

If your loved ones depends in your work for healthcare, take discover. In keeping with eHealth.com, the typical medical health insurance premium for a household is $22,221. That’s a shade underneath $2,000 monthly in extra price. This price will solely rise, and the necessity might final for years.

Different Obligations You Could Must Cowl

Up to now, we’ve been describing the monetary obligations prone to have an effect on a typical family.

However there could also be sure conditions that can produce obligations which can be much less apparent.

Enterprise Homeowners

For instance, should you’re a enterprise proprietor, there could also be money owed or different monetary obligations that can have to be paid upon your loss of life.

Though nobody in your loved ones could also be certified or all in favour of taking on your enterprise, the payoff of these obligations could also be utterly essential to allow the sale of the enterprise.

Actual Property Investor

One other risk is that you just’re an actual property investor.

In case your properties are closely indebted, additional insurance coverage proceeds could also be vital both to hold the properties till they’re bought, and even to repay present indebtedness to liberate money move for earnings.

You could even want extra funds if you're caring for an prolonged member of the family,like an ageing dad or mum.

These are simply among the many potentialities of bills that can have to be coated by insurance coverage proceeds.

Components Affecting Your Life Insurance coverage Premiums

Earlier than we transfer on to particular life insurance coverage quotes,let’s first contemplate the components that have an effect on time period life insurance coverage premiums.

Age

That is usually the one most necessary premium issue. The older you might be,the extra doubtless you might be to die inside the time period of the coverage.

Well being

It is a shut second and why it’s so necessary to use for a coverage as early in life as potential. Premiums on life insurances charges actually improve by every year.

If in case you have any well being situations that will have an effect on mortality,equivalent to diabetes or hypertension,your premiums shall be greater. That is one other compelling motive to use while you're younger and in good well being.

It’s not that insurance policies should not accessible to individuals with well being situations, it’s simply that they’re inexpensive should you don’t have any.

Coverage Time period

A ten-year time period coverage can have a decrease premium than a 20-year time period coverage, which shall be decrease than a 30-year time period. The shorter the time period, the much less doubtless it's the insurance coverage firm must pay a declare earlier than it expires.

Coverage Dimension

Dimension of the coverage issues,however not the way in which you may assume. Sure,a $1 million coverage will price greater than a $500,000 coverage. Nevertheless it received’t price twice as a lot.

The bigger the coverage,the decrease the per-thousand price shall be.

When the dimensions of the loss of life profit is taken into account,the bigger coverage will at all times be cheaper.

Work,Hobbies,and Habits

For instance,sure occupations are extra hazardous than others (assume policeman versus librarian). Deep-sea diving is greater danger than golf. And smoking is the one exercise assured to boost your premiums considerably.

With this info in thoughts,let’s check out whether or not you need to contemplate a $1 million complete life coverage as an alternative.

$1 Million Time period Life Insurance coverage vs Entire Life?

Any dialogue on life insurance coverage ought to embrace a comparability of complete life and time period life insurance coverage protection. In spite of everything,each merchandise may be immensely beneficial in the proper state of affairs,but one product (complete life) prices significantly greater than the opposite.

More often than not,the controversy is settled in favor of time period life insurance coverage primarily based on price alone.

With that being mentioned,complete life insurance coverage and different investment-type life insurance coverage protection may be beneficial when it comes to the money worth you possibly can construct up over time. Entire life insurance coverage additionally gives a hard and fast profit quantity in your heirs that can final in your total life,but the price of your premiums are assured to remain the identical.

The money worth of a complete life insurance coverage coverage additionally grows on a tax-deferred foundation,and you may borrow in opposition to this quantity should you want a mortgage. Additional,many complete life insurance policies from respected suppliers additionally pay out dividends throughout good years,which may be substantial.

Why Younger Households Select Time period Protection

The issue with complete life and different related insurance policies like common life is the truth that premiums may be exorbitant for the quantity of protection you may want.

A pair with younger kids offers a very good instance since they could want a $1 million greenback coverage or extra to supply earnings safety for his or her working years and have cash left for faculty tuition and different bills.

With younger households,bills are already excessive.

This contains prices for meals for a household,childcare,heavy use of well being care,and the seemingly infinite demand for clothes,furnishings,and even leisure as the youngsters develop.

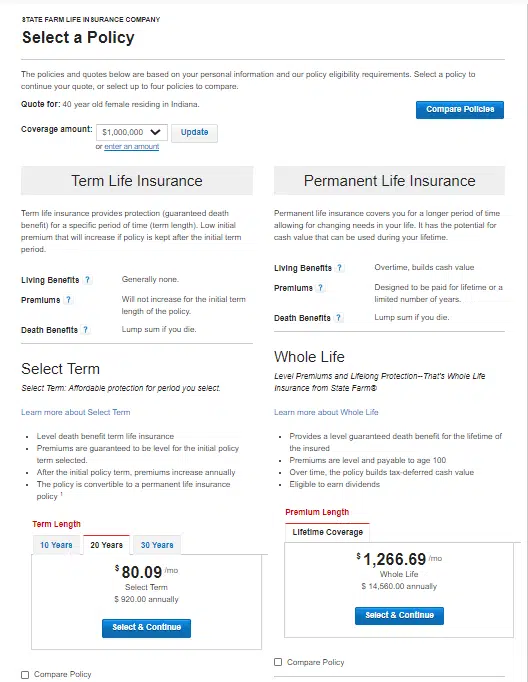

As you possibly can see from the associated fee comparability beneath from State Farm,there’s not sufficient room within the typical household price range to afford the sort of life insurance coverage that’s wanted.

A 40-year-old mom and breadwinner in glorious well being would pay $80.09 monthly for a time period life coverage that lasts 20 years,whereas a complete life coverage in the identical quantity would price $1,266.69 monthly (or $14,560 yearly).

It is a basic state of affairs the place time period insurance coverage rides to the rescue. The household can afford to purchase the quantity of protection they want at an reasonably priced worth,whereas paying for everlasting life insurance coverage protectionin the identical quantity can be troublesome to justify.

And simply as necessary for individuals of any age and in any circumstance,the additional funds not being spent on insurance coverage premiums may be invested to regularly enhance your monetary state of affairs.

So completely,time period insurance coverage will work finest for most individuals.

$1 Million Life Insurance coverage Charge Examples

As you’ll discover,every desk has a big selection of knowledge. Understanding that everyone is in a special state of affairs,I needed to ensure that I provided time period life quotes for nearly each conceivable state of affairs.

I’ve included life insurance coverage charges for a 30-year time period,20-year time period,and a 10-year time period million greenback life insurance policies. Should you’re a tobacco person,I’ve additionally included some quotes from life insurance coverage for people who smoke.

30-12 months $1 Million Time period Life Coverage

For people who assume{that a}million-dollar time period coverage is dear,you’ll rapidly discover{that a}25-year-old male in good well being solely prices $645 per yr whereas a 35-year-old prices $795.

On a month-to-month foundation that’s virtually subsequent to nothing!

| AGE | SEX | COMPANY 1 | COMPANY 2 | COMPANY 3 |

|---|---|---|---|---|

| 25 | MALE | BANNER LIFE $645 | NORTH AMERICAN CO. $645 | TRANSAMERICA $650 |

| 25 | FEMALE | AMERICAN GENERAL $514 | NORTH AMERICA CO. $515 | SBLI $520 |

| 35 | MALE | BANNER LIFE $795 | GENWORTH FINANCIAL $804 | ING $808 |

| 35 | FEMALE | SBLI $640 | AMERICAN GENERAL $694 | GENWORTH FINANCIAL $695 |

| 45 | MALE | BANNER LIFE $1,885 | GENWORTH FINANCIAL $1891 | AMERICAN GENERAL $1,894 |

| 45 | FEMALE | SBLI $1,450 | BANNER LIFE $1,455 | AMERICAN GENERAL $1,456 |

20-12 months $1 Million Time period Life Coverage

There's a huge drop-off in life insurance coverage charges between a 20 yr and a 30 yr since underwriters wouldn't have to fret as a lot about life expectancy.

For many individuals,a 20-year coverage will get them precisely the place they need to be in life when the coverage time period runs out.

| AGE | SEX | COMPANY 1 | COMPANY 2 | COMPANY 3 |

|---|---|---|---|---|

| 25 | MALE | AMERICAN GENERAL $414 | BANNER LIFE $425 | SBLI $440 |

| 25 | FEMALE | AMERICAN GENERAL $354 | SBLI $360 | BANNER LIFE $365 |

| 35 | MALE | SBLI $450 | BANNER LIFE $455 | NORTH AMERICA CO. $485 |

| 35 | FEMALE | SBLI $390 | AMERICAN GENERAL $404 | BANNER LIFE $405 |

| 45 | MALE | BANNER LIFE $1,155 | SBLI $1,160 | GENWORTH FINANCIAL $1,173 |

| 45 | FEMALE | SBLI $880 | BANNER LIFE $895 | TRANSAMERICA $930 |

10-12 months $1 Million Time period Life Coverage

As soon as once more,you get a $200 drop within the annual premium by shedding one other 10 years on the time period.

In case your life insurance coverage agent isn’t providing you with all these time period choices and is simply centered on the loss of life profit,then you definately want a special agent.

| AGE | SEX | COMPANY 1 | COMPANY 2 | COMPANY 3 |

|---|---|---|---|---|

| 25 | MALE | SBLI $260 | BANNER LIFE $285 | MINNESOTA LIFE $290 |

| 25 | FEMALE | SBLI $230 | BANNER LIFE $245 | ING $248 |

| 35 | MALE | SBLI $270 | BANNER LIFE $295 | MINNESOTA LIFE $300 |

| 35 | FEMALE | SBLI $240 | BANNER LIFE $255 | ING $258 |

| 45 | MALE | BANNER LIFE $585 | TRANSAMERICA $630 | GENWORTH FINANCIAL $637 |

| 45 | FEMALE | SBLI $520 | BANNER LIFE $525 | ING $528 |

$1 Million Coverage for People who smoke – Charges Enhance

For all you people who smoke on the market – beware! The price of your life insurance coverage balloons as you’ll see right here. Should you’re contemplating kicking the behavior,now's nearly as good time as any.

Some life insurance coverage firms offers you a decrease fee should you full a acknowledged smoking cessation program, and go on with out smoking for no less than two years.

It received’t assist your instant state of affairs, however once you see the premium on smoker life insurance coverage charges beneath, you may agree that it’s one thing to work towards!

| AGE | SEX | COMPANY 1 | COMPANY 2 | COMPANY 3 |

|---|---|---|---|---|

| 35 | MALE | North American Co. $3595 |

SBLI $3630 |

MetLife $3639 |

| 35 | FEMALE | North American Co. $2555 |

Transamerica $2720 |

Prudential $2765 |

10 steps to securing one million life insurance coverage coverage:

Should you’ve made the choice that $1 million of life insurance coverage is the correct amount of protection you want and also you’re able to buy a coverage, listed here are the steps you’ll have to comply with.

1. Decide How A lot Protection You Want: That is the primary and most necessary step in securing one million life insurance coverage insurance policies. You have to have a transparent understanding of how a lot protection you really want.

2. Select the Proper Kind of Coverage: There are complete life, time period life, and Common life insurance policies accessible. Select the one which most closely fits your wants.

3. Store Round: Don’t simply go along with the primary life insurance coverage firm you come throughout. It’s necessary to match life insurance coverage charges and protection from a number of totally different firms earlier than making a choice.

4. Contemplate Your Well being: Should you’re in good well being, you’ll doubtless qualify for decrease charges. Nonetheless, you probably have well being points, you should still have the ability to get protection, however it is going to most likely be dearer.

5. Contemplate Your Way of life: If in case you have a dangerous job or interest, that might have an effect on your charges.

6. Get Quotes From A number of Firms: That is one of the best ways to match charges and discover the most affordable coverage.

7. Learn the Positive Print: Ensure you perceive all of the phrases and situations of the coverage earlier than shopping for it.

8. Purchase On-line: You'll be able to often get cheaper charges by shopping for life insurance coverage on-line.

9. Pay Consideration to Your Cost Schedule:Most life insurance coverage insurance policies require month-to-month or annual funds. Make certain you possibly can afford the funds earlier than shopping for a coverage.

10. Evaluate Your Coverage Recurrently:Life modifications,and so do life insurance coverage wants. You should definitely evaluation your coverage often to verify it nonetheless meets your wants.

Following these steps will provide help to get the very best fee on a million-dollar life insurance coverage coverage.

Ensure you perceive all of the phrases and situations earlier than signing on the dotted line. Additionally,be certain to buy round and examine charges from a number of firms earlier than shopping for a coverage.

Sure,I do know I’ve mentioned that a number of occasions on this article,nevertheless it’s value repeating. Many individuals go along with the primary life insurance coverage firm they name,and that isn’t type to their checkbook. It pays to buy round.

Right here’s what it's worthwhile to learn about selecting the perfect life insurance coverage firm in your $1 million coverage:

The Greatest Firms to Buy $1 Million Life Insurance coverage

When selecting the perfect life insurance coverage firm, it’s necessary to contemplate the total monetary well being of the insurance coverage firm. You need to be certain the corporate you select is steady and shall be round for years to return. You additionally need to contemplate issues like the corporate’s customer support ranking and claims-paying skill.

There are quite a lot of totally different life insurance coverage firms on the market, so it may be troublesome to know which one is the perfect. Every firm is rated by totally different organizations, so it’s necessary to take a look at a number of scores earlier than making a choice.

The businesses that fee insurance coverage firms are A.M. Greatest, Moody’s, and Normal & Poor’s.

A.M. Greatest is a credit standing company that makes a speciality of the insurance coverage business. They fee insurance coverage firms on their monetary stability.

Moody’s is one other credit standing company. In addition they fee insurance coverage firms on their monetary stability.

Normal & Poor’s is a credit standing company that charges firms on their monetary stability.

The next life insurance coverage firms are all rated A+ (Superior) by A.M. Greatest and are thought of to be financially steady and have a very good claim-paying skill.

1. Northwestern Mutual

2. New York Life

3. MassMutual

4. Guardian Life

5. State Farm

6. Nationwide

7. USAA

8. MetLife

9. The Hartford

10. Allstate

Listed below are those self same high life insurance coverage firms with their respective scores:

| Firm | AM Greatest | Moody’s | Normal & Poor’s |

| Northwestern Mutual | A++ | Aaa | AA+ |

| New York Life | A++ | Aaa | AA+ |

| MassMutual | A++ | A2 | AA+ |

| Guardian Life | A++ | Aa2 | AA+ |

| State Farm | A++ | A1 | AA |

| Nationwide | A+ | A1 | A+ |

| USAA | A++ | Aa1 | AA+ |

| MetLife | A- | A3 | A- |

| The Hartford | A+ | A1 | A+ |

| Allstate | A+ | A3 | A- |

These are just some of the various life insurance coverage firms on the market that might offer you a $1 million life insurance coverage coverage.

When selecting a life insurance coverage firm, it’s necessary to contemplate their monetary stability, customer support ranking, and claims-paying skill. The businesses listed above are all rated A+ (Superior) by A.M. Greatest and are thought of to be financially steady with a very good claims-paying skill.

Northwestern Mutual, New York Life, MassMutual, Guardian Life, State Farm, Nationwide, USAA, MetLife, The Hartford, and Allstate are all good selections for all times insurance coverage firms.

You'll be able to’t put a worth on peace of thoughts,and with a $1 million life insurance coverage coverage you possibly can have the peace of thoughts understanding that your family members shall be taken care of financially if one thing occurs to you.

Backside Line:How A lot Does A $1 Million Greenback Life Insurance coverage Coverage Value?

Getting a one-million-dollar time period life insurance coverage coverage will not be as costly as most individuals imagine. You can begin getting quotes right this moment from quite a lot of high life insurers by choosing your state from the map above.

Even those that go for the dearer everlasting life insurance coverage coverage will many occasions be stunned on the worth.

Both approach,you may get these bigger quantities of protection and nonetheless not break the financial institution. However get your coverage now,when you’re nonetheless younger and in good well being.

FAQ’s on $1 Million Life Insurance coverage Coverage

The price of a $1,000,000 life insurance coverage coverage will differ primarily based on components like your age,well being,and life-style. Nonetheless,you possibly can count on to pay round $250 per yr for a wholesome 30-year-old. In keeping with Ladder Life,a $1 million time period life coverage for wholesome 30-year-old males prices round $2.08 per day.

A $1 million time period life insurance coverage coverage is a sort of life insurance coverage that gives protection for a particular time period,often 10-20 years. Should you die throughout the time period of the coverage,your beneficiaries will obtain a loss of life advantage of $1 million. Should you dwell previous the time period of the coverage,the coverage will expire and you'll not obtain any loss of life profit.

A $1 million time period life insurance coverage coverage is an effective alternative for individuals who need to be certain their family members are taken care of financially if one thing occurs to them. It may also be a good selection for individuals with quite a lot of debt, like a mortgage or scholar loans, that they need to be certain is paid off in the event that they die.

For essentially the most half, sure; however there are examples of people that can't purchase life insurance coverage. For example,individuals with a terminal sickness or those that have been recognized with a life expectancy of fewer than two years should not in a position to buy life insurance coverage insurance policies.

The opposite components are your earnings,affordability,and suitability. Should you can't afford the premiums, then you definately won't be able to buy the coverage. And in case your earnings is say lower than $50,000 then the insurance coverage firm could not assume it’s appropriate to buy a $1 million life insurance coverage coverage.

One million-dollar life insurance coverage coverage might not be proper for everybody,however it may be a good suggestion you probably have quite a lot of debt or if you wish to be certain your loved ones is taken care of financially if one thing occurs to you.

Nobody likes to consider their loss of life,nevertheless it’s necessary to have a life insurance coverage coverage in place in case one thing occurs to you. One million-dollar life insurance coverage coverage may give you and the one you love’s peace of thoughts understanding that they are going to be taken care of financially if one thing occurs to you.

There isn't any one-size-fits-all reply to this query, as the perfect coverage for you'll rely in your particular wants and preferences. Nonetheless,among the high suppliers of million-dollar life insurance coverage insurance policies embrace AIG,Banner Life,and Prudential. So you should definitely discover your choices and examine quotes from totally different suppliers earlier than making a choice.

Sure,insurance coverage firms provide million-dollar insurance coverage insurance policies with no medical examination. Nonetheless,the premiums for these insurance policies are usually a lot greater than for insurance policies with a medical examination.