{kind=link}

A reader asks:

Ben shared a chart in a current episode that exhibits nationwide housing costs not often ever fall within the U.S. That makes me really feel a little bit higher about my spouse and I (each 29) shopping for our first dwelling. However isn’t right now a horrible time to purchase a house from an funding perspective as a result of costs are a lot greater? What ought to we be contemplating when taking a look at this by an funding lens (understanding full effectively there are different causes to purchase a home)?

The conundrum posed on this query seems to be one thing like this:

Housing affordability isn’t good as a result of we pulled ahead a decade’s price of positive aspects right into a 3 yr window.

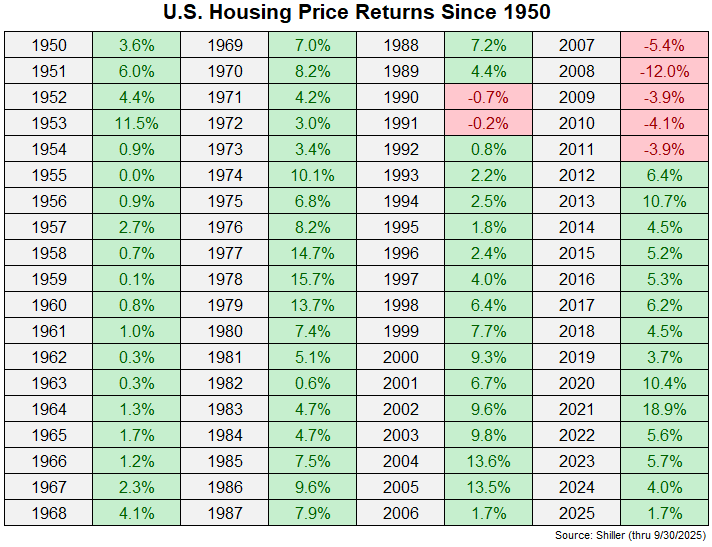

Nonetheless, housing costs have not often gone down traditionally. Right here’s the chart talked about (from this weblog publish):

Housing costs merely don’t fall that always on a nationwide foundation.

The true query right here is how will we sq. the present knowledge with the historic knowledge? Do you have to hear to the current or the previous?

As at all times, a very powerful distinction with each funding is the time horizon. How lengthy do you intend to personal the home for?

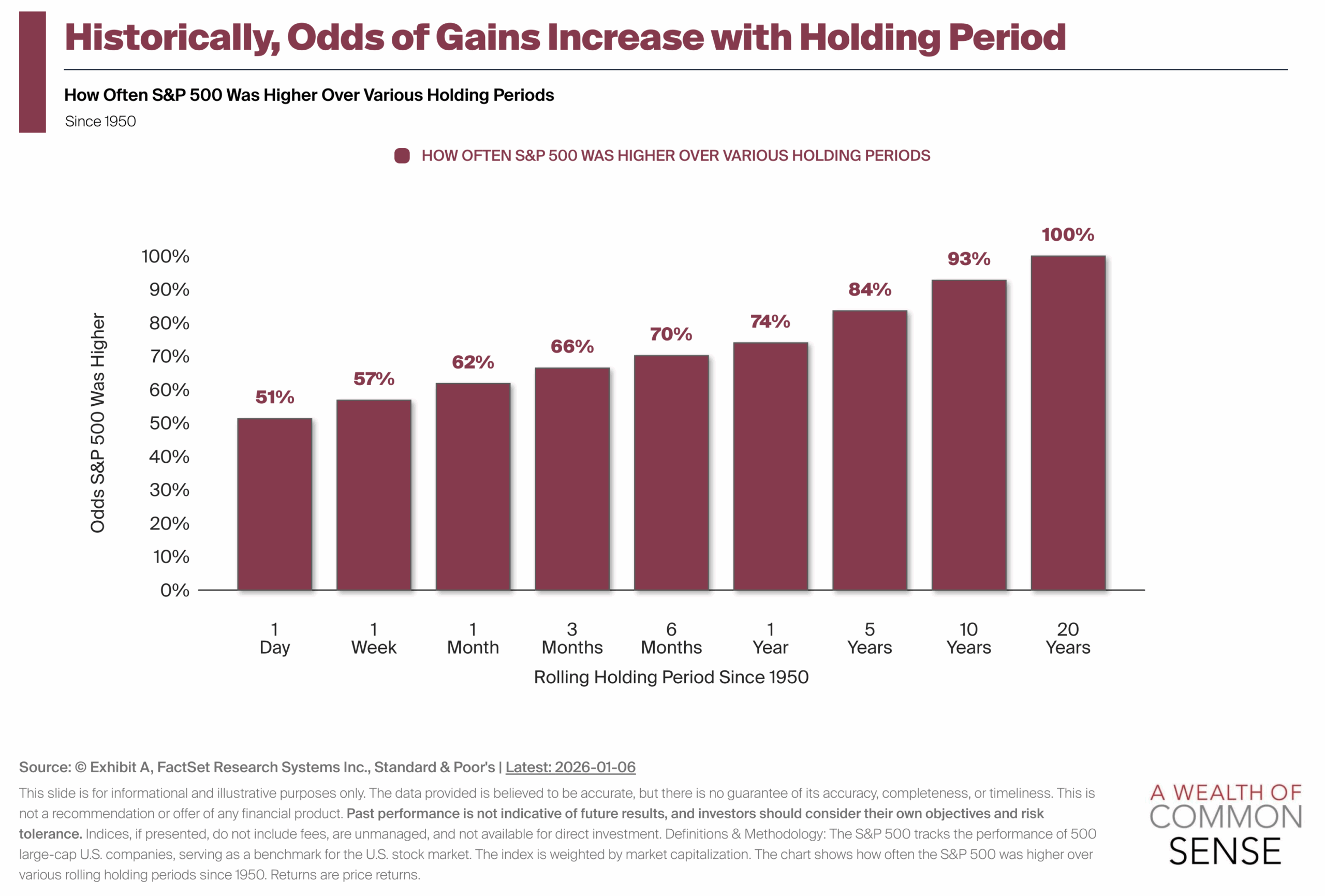

Considered one of my favourite charts seems to be on the win charge for the inventory market by holding interval:

The inventory market is the most effective on line casino on the planet. The longer you play, the upper your odds of strolling away a winner, the other of an precise on line casino.

I had by no means checked out this knowledge earlier than relating to housing. Right here’s what it seems to be like going again to the Fifties:

Fairly spectacular. That’s a a lot greater win charge than the inventory market throughout the board.

In fact, your anticipated returns are decrease within the housing market and there isn’t as a lot volatility so these outcomes make sense in principle in addition to observe.

It’s additionally price noting that these numbers don’t embrace the entire ancillary prices like realtor charges, property taxes, closing prices, insurance coverage, upkeep, and many others.

However these frictional prices are why your time horizon is much more vital within the housing market than the inventory market. You don’t need to be leaping out and in of actual property offers as a result of the prices will eat up the majority of your positive aspects.

I don’t know what’s going to occur with housing costs from right here.

It wouldn’t shock me in the event that they stagnate for a number of years whereas incomes play catch-up to even our affordability. Or possibly they may merely sustain with inflation. Who is aware of? Possibly inflation and/or demographics push housing costs even greater.

The 2020s are an ideal instance of how unknowable housing value returns might be. Nobody may have presumably predicted a housing growth due to a pandemic.

In lieu of a crystal ball, listed below are some issues for those who’re apprehensive concerning the funding aspect of issues when shopping for a home within the present atmosphere:

You might use a smaller down cost. For those who’re apprehensive about housing as an funding, you would possibly put down 5-10% as an alternative of 15-20%.1

This could contain borrowing more cash nevertheless it’s much less up entrance in an asset that you simply suppose would possibly wrestle within the years forward. That method you may preserve cash in different danger property as effectively.

Leverage cuts each methods however my first down cost was simply 5% and I used to be positive with that.2

You might skip the starter dwelling. I’ve by no means been an enormous fan of starter properties due to all the prices concerned in actual property transactions.

I don’t like the thought of shopping for a home, possibly placing some cash into it after which hoping to promote it 3-5 years sooner or later to be able to commerce up. Most of your fairness will get eaten up by realtor charges, closing prices and the heavy up-front curiosity expense in your mortgage.

For those who can afford it, I want paying up for a greater dwelling you possibly can see your self dwelling in for a for much longer time-frame.

You might reside in the home longer. The most effective funding recommendation usually boils right down to lengthening your time horizon. May housing be a nasty funding for the subsequent few years? Yeah it may.

For those who plan on dwelling in the home for 10+ years I don’t suppose you’ll remorse it.

A very powerful factor is your means to service the mortgage debt and deal with all of the ancillary prices of homeownership.

If you are able to do that whereas dwelling in your required neighborhood and derive some psychological advantages then it’s price it.

For those who can’t abdomen the potential of doubtlessly dwelling in a nasty funding, homeownership may not be for you.

I coated this query on an all-new episode of Ask the Compound:

My favourite CFO, Invoice Candy, joined us on the present once more this week to reply questions on Roth 401ks, utilizing margin in your portfolio, balancing retirement accounts and the way a 22-year-old ought to save for retirement. Plus we requested Invoice a bunch of tax questions to arrange for the brand new yr.

Additional Studying:

Will House Costs Lastly Fall in 2026?

1Assuming your monetary establishment permits it.

2It was additionally all we may afford on the time.