{kind=link}

Bonds had a stable begin to 2025, with most high-quality mounted earnings sectors up low- to mid-single digits by way of the primary half of the 12 months. Whereas shares skilled a roller-coaster experience powered by coverage uncertainty, mounted earnings typically held up nicely regardless of the broader market turbulence. Will or not it’s the identical story within the second half? Let’s take a better look.

A Flock to Security

Traditionally, investment-grade bonds have benefited in occasions of uncertainty, as traders typically flock to the protection of high-quality mounted earnings when dangers rise. We actually noticed that play out earlier this 12 months when shares offered off and bonds rallied. The chart beneath highlights year-to-date and one-year returns for a handful of main sectors inside mounted earnings.

Yr-to-Date and 1-Yr Whole Returns

| Yr-to-Date | 1 Yr | |

| Bloomberg U.S. Combination Bond Index | 2.35% | 4.61% |

| Bloomberg U.S. Company Bond Index | 2.40% | 5.13% |

| Bloomberg U.S. Company Excessive Yield Index | 3.10% | 9.26% |

| Bloomberg Municipal Bond Index | -1.02% | 0.91% |

| Bloomberg Municipal Excessive Yield Bond Index | 2.47% | 5.54% |

| Bloomberg U.S. Treasury 1-5 Yr Index | 3.44% | 6.45% |

Supply: Bloomberg, as of 6/10/2025. All indices are unmanaged, and traders can not really make investments straight into an index. In contrast to investments, indices don’t incur administration charges, fees, or bills. Previous efficiency doesn’t assure future outcomes.

Wanting ahead to the second half of the 12 months, the more than likely consequence for mounted earnings traders is sustained stable features. Nonetheless, there are dangers that ought to be acknowledged and monitored, together with the menace to the bond rally posed by growing issues in regards to the nation’s deficit and long-term debt plans.

Shifting Focus to Lengthy-Time period Yields

When will the Fed begin chopping charges? Coming into the 12 months, that was one of many main questions for the bond market. We entered the 12 months with merchants pricing between one and two rate of interest cuts in 2025, with the primary minimize anticipated in Might as a consequence of an anticipated financial slowdown. However this price minimize by no means materialized. The financial knowledge confirmed the job market remained impressively resilient by way of the beginning of the 12 months, whereas inflation remained stubbornly excessive. Fed members, together with Chair Jerome Powell, have indicated the central financial institution is in no rush to regulate rates of interest and can stay data-dependent when setting charges at future conferences.

Given the dearth of Fed exercise to begin the 12 months and muted expectations for additional price cuts in 2025, investor focus has shifted towards the longer finish of the yield curve. This shift turned particularly obvious after Moody’s downgrade of the U.S. economic system in Might amid the continued congressional budgeting discussions which are set to broaden the scale of the deficit and nationwide debt.

Lengthy-term Treasury yields fell all through the primary quarter of the 12 months. Within the second quarter, they rose notably, with the 30-year Treasury yield hitting a latest excessive of practically 5.10 p.c in late Might. Whereas long-term yields have pulled again modestly from latest highs, they nonetheless sit nicely above the degrees seen all through 2024, indicating continued investor concern. Upwards strain on long-term yields might current a headwind for mounted earnings traders within the second half of the 12 months, particularly as congressional negotiations over the finances and tax insurance policies proceed.

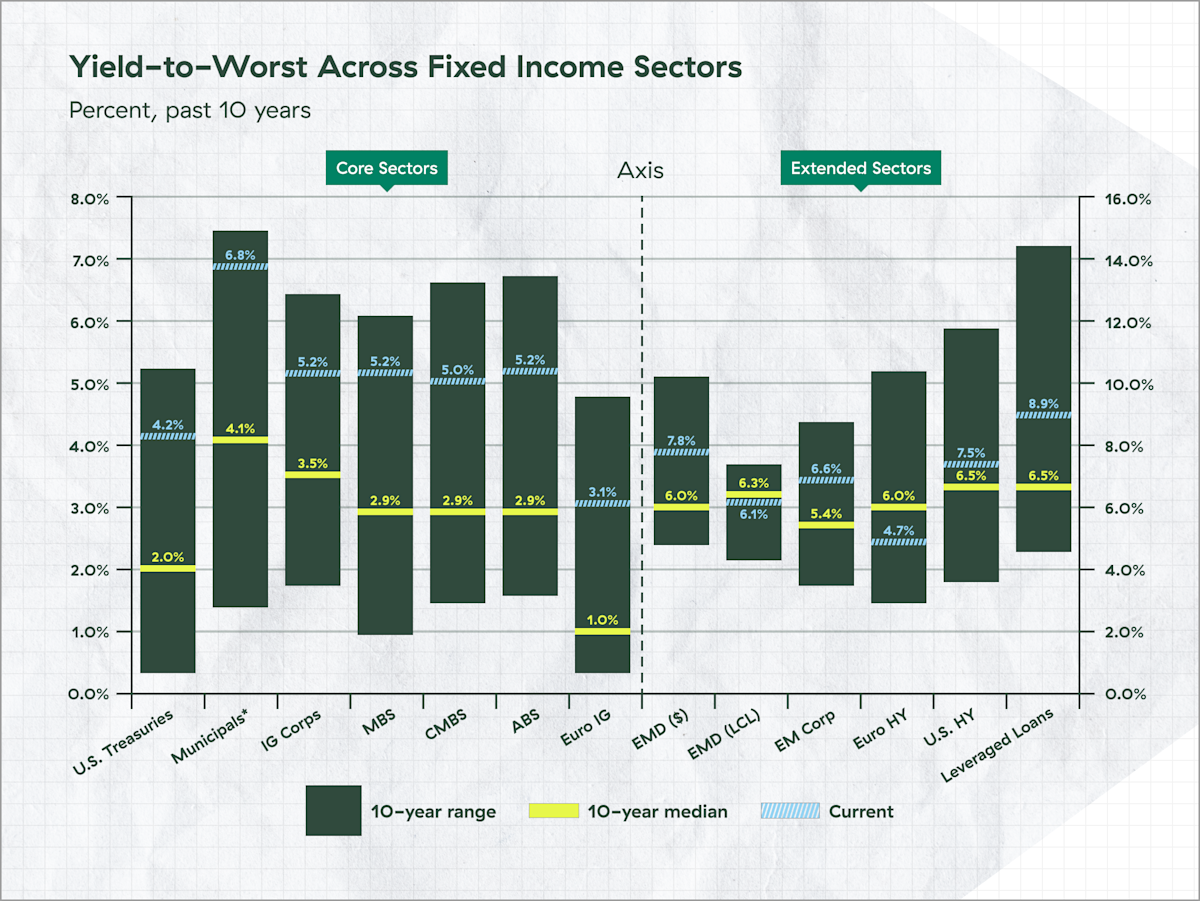

A Have a look at Company and Municipal Bonds

Whereas Treasury yields attracted a lot of the consideration within the first half of the 12 months, there are compelling alternatives within the company and municipal bond markets for traders prepared to tackle credit score threat in change for heightened yields.

Treasury, municipal, and company bond yields are all at the moment above their respective 10-year median values (see chart beneath). However tax-adjusted municipal bonds and investment-grade company bonds might present extra potential yield in comparison with Treasuries.

Supply: Bloomberg, FactSet, J.P. Morgan Credit score Analysis, J.P. Morgan Asset Administration. Indices used are Bloomberg apart from ABS, rising market debt and leveraged loans: ABS: J.P. Morgan ABS Index; CMBS: Bloomberg Funding Grade CMBS Index; EMD (USD): J.P. Morgan EMIGLOBAL Diversified Index; EMD (LCL): J.P. Morgan GBI-EM International Diversified Index; EM Corp.: J.P. Morgan CEMBI Broad Diversified; Leveraged Loans: JPM Leveraged Mortgage Index; Euro IG: Bloomberg Euro Combination Company Index; Euro HY: Bloomberg Pan-European Excessive Yield Index. Yield-to-worst is the bottom attainable yield that may be acquired on a bond aside from the corporate defaulting and considers components like name provisions, prepayments and different options that will have an effect on the bonds’ money flows. *All sectors proven are yield-to-worst apart from Municipals, which is predicated on the tax-equivalent yield-to-worst assuming a top-income tax bracket price of 37% plus a Medicare tax price of three.8%. Information to the Markets – U.S. Knowledge are as of Might 30, 2025.

Whereas investment-grade company bonds have moved according to the broader market thus far this 12 months, investment-grade municipal bond returns lagged their friends within the first half. This underperformance was largely as a consequence of a mix of excessive issuance and uneven funding flows, together with issues about potential tax coverage modifications that might strip some municipal issuers of their tax-exempt standing. Wanting ahead, these headwinds are anticipated to show into tailwinds for traders, as municipal bond valuations seem comparatively engaging as a result of latest underperformance.

Bonds Performing Like Bonds

Finally, the primary half of the 12 months was largely constructive for mounted earnings traders. Regardless of the ups and downs for shares, bonds held up comparatively nicely compared. Given the coverage volatility to begin the 12 months, it’s encouraging to see bonds appearing like bonds in occasions of market uncertainty. We must always count on to see that conduct proceed within the second half.

That’s to not say there aren’t any dangers to this outlook. Political uncertainty stays essentially the most urgent subject for traders. Whereas we’ve seen progress in decreasing the temperature of the continued finances and commerce negotiations, additional surprises or disruptions might rattle markets. Mounted earnings traders may additionally face financial headwinds, particularly if there’s a sustained rise in inflationary strain.

Whereas high-quality bonds have traditionally carried out nicely in occasions of uncertainty, latest historical past has proven intervals the place bonds and shares skilled declines on the similar time. Most just lately, in 2022, a surge in inflation and rates of interest led to double-digit losses for each shares and bonds. Whereas it’s not anticipated right now, if we do see a significant rise in inflation, it might negatively affect markets, particularly if it prevents the Fed from decreasing charges later within the 12 months.

Cautious Optimism Forward

All that being mentioned, mounted earnings traders ought to be cautiously optimistic as we enter the second half of the 12 months. Valuations are stable, yields are compelling, and bonds are appearing like bonds once more. These components ought to contribute to a stable remainder of the 12 months for traders.

Bonds are topic to availability and market circumstances; some have name options that will have an effect on earnings. Bond costs and yields are inversely associated: when the value goes up, the yield goes down, and vice versa. Market threat is a consideration if offered or redeemed previous to maturity.