{kind=link}

A reader asks:

I’ve $1.6M in a taxable brokerage account, $250k in a standard 401k and one other $150k in money. No debt. No home. I’m single with no dependents. I want $170k in annual earnings to retire. At a 4% withdrawal charge I’d want $4.25M to fulfill that earnings aim. Lately, lined name funds have develop into in style. For instance, SPYI “yields” 12%. Which means $1.4M invested would yield $170k per yr. Is that this too good to be true? Why is that this a foul concept? I’m 42 years previous and depressing. I personal a small enterprise and have labored almost on daily basis for over a decade. I don’t know if I can do it anymore. I’m completely burned out and wish to be carried out with it.

The investing query right here is an attention-grabbing thought train from a numbers perspective however the small enterprise angle is way extra vital from a human perspective.

Let’s begin with the numbers since that’s the easier a part of the equation.

I’ve written about lined name methods earlier than. Right here’s the reason I gave a couple of years in the past:

A name possibility is a contract that offers the client the precise to buy a safety at a predetermined worth in some unspecified time in the future on or earlier than a predetermined date. The vendor of that decision possibility has an obligation to promote the safety at that predetermined worth if it occurs to make it there by the predetermined date.

If the inventory by no means reaches the strike worth in that time-frame, the client is simply out the premium paid whereas the vendor retains the choice premium regardless.

For instance, let’s say you personal 50 shares of a inventory that’s at the moment buying and selling for $20. Name choices with a strike worth of $25 value 50 cents a chunk so you’ll earn $25 in earnings in your $1,000 place. That’s adequate for a yield of two.5%.

However now your upside is proscribed to a 25% achieve (going from $20 to $25) plus that 2.5% possibility premium.

If the inventory goes to $30 or $35 you’re out these extra beneficial properties over and above $25 and the choice purchaser is out their $25 in premiums.

In a lined name technique, you’re the vendor of name choices in your particular person holdings or an index.

Thus, that is the kind of technique that ought to underperform in a rip-roaring bull market. The earnings from the sale of choices may also help however in a hard-charging bull market however you’ll probably miss out on some beneficial properties and lag the general market.

Nevertheless, in a bear market, this technique ought to outperform the market as a result of the choice earnings acts as a buffer. Plus, in a bear market, volatility spikes which ought to really enhance your earnings since volatility performs a big position within the pricing of choices.

Lined name funds turned all the trend following the 2022 bear market due to the truth that they outperformed in a down market and include excessive yields as well.

Lined name methods are completely cheap as a strategy to cut back fairness volatility and enhance your earnings. However you must perceive how these funds work in relation to the earnings part.

The yield on a lined name technique isn’t the Holy Grail many assume it’s. You’re not essentially defeating the 4% rule simply because the yield is so excessive. It’s essential to contemplate complete return, not simply the earnings part.

For instance, check out the distinction between the worth return and complete return on a handful of the most important lined name methods:

The entire returns are fairly good over the previous few years. However have a look at the worth returns. They’re primarily unchanged.

This tells you that mainly all the return has come from the yield. There’s nothing unsuitable with that per se, except you intend on dwelling on the earnings. When you’re spending the yield part of those funds and never reinvesting it then inflation turns into an enormous danger.

That is very true for those who’re making an attempt to retire in your 40s. A 3% inflation charge would make one greenback right now value 40 cents in 30 years.

Your earnings additionally turns into way more variable in these funds. Lined name methods ought to fall lower than the general market throughout a downturn due to the earnings part however they nonetheless personal shares. In the course of the Liberation Day sell-off final yr these funds have been down wherever from 16% to 22%.

In a chronic bear market, your earnings goes down too.

Lined calls may completely play a job within the earnings portion of your portfolio however there’s extra to it than the listed yield.

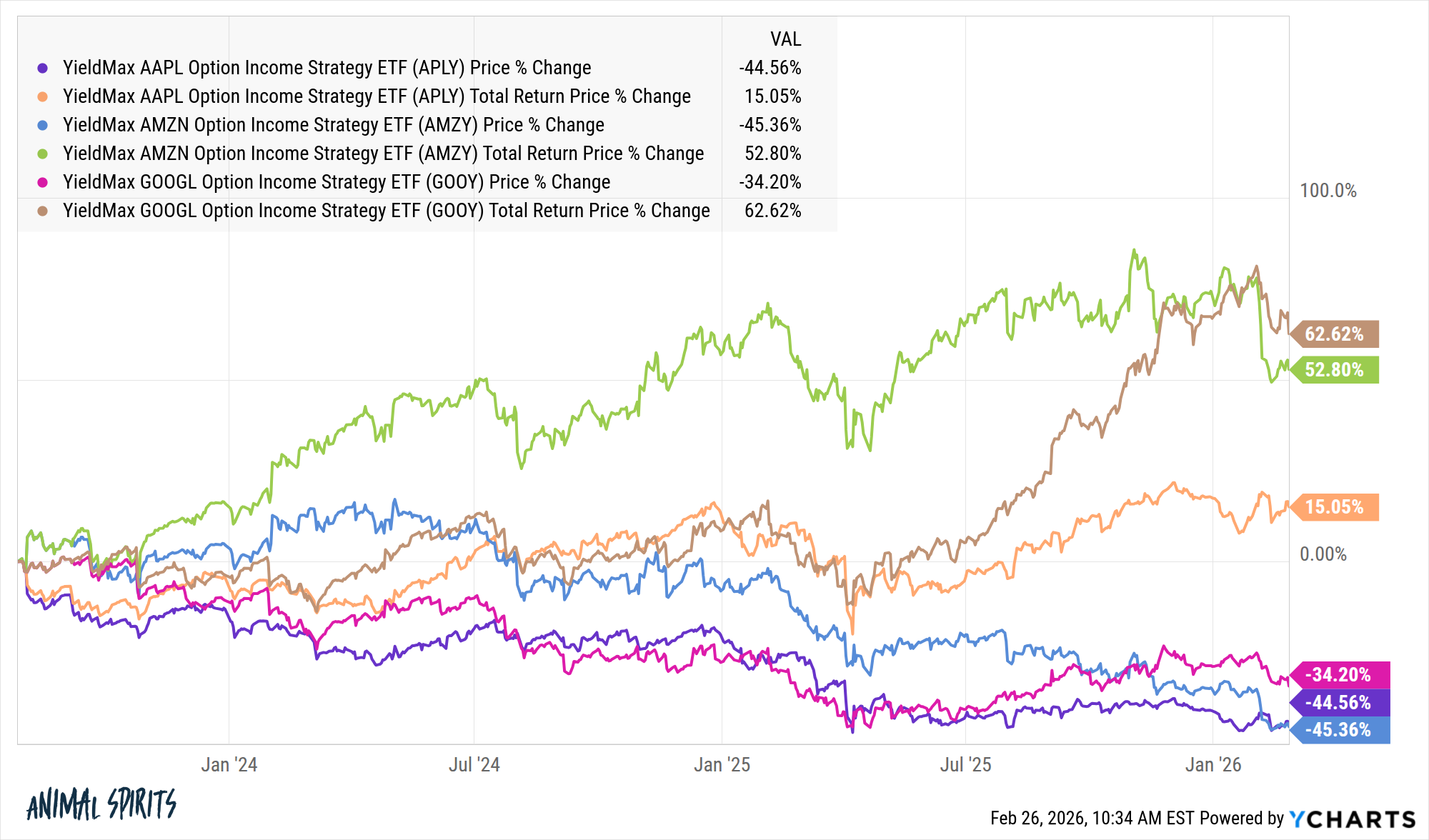

I might be remiss if I didn’t point out the one inventory lined name methods which have develop into all the trend lately. YieldMax has ETFs that promote calls on particular person shares. Proper now the lined name ETFs for Amazon, Google and Apple yield 43%, 39% and 37%, respectively.

Sounds nice, proper?

Have a look at the distinction between worth and complete returns for these funds:

There isn’t a free lunch. Larger yields imply increased danger. And danger by no means utterly goes away both.

The excellent news is you’re 42 years previous, value $2 million and haven’t any debt. That’s an enormous accomplishment.

The dangerous information is you’re working an excessive amount of and it’s making you depressing.

This can be a good reminder that working your personal enterprise could be extremely profitable but additionally requires a ton of labor.

If you wish to spend $170k a yr on a $2 million portfolio, that’s a withdrawal charge of 8.5%. There’s no margin of security at your age as a result of the cash has to final you a really very long time.

You can flip down the dial in your spending.

You can attempt to promote the enterprise.

You can rent a supervisor for the enterprise and extract your self from the day-to-day.

With no dependents, you find the money for to take a yr or two off to determine what you wish to do subsequent.

Perhaps you don’t find the money for to dwell off the dividends at your present spending charge however you have got loads of cash to take a break and reassess what you wish to do along with your life.

Cash won’t have the ability to make you happier however it could make you extra comfy and relieve some stress.

That ought to be your aim.

Invoice Candy helped me deal with this query on an all-new Ask the Compound:

We additionally answered questions on field unfold loans, retirement plans for small companies, Coast FIRE and tax-efficient asset location methods.

Additional Studying:

Can Lined Name Choices Function a Bond Alternative?