{kind=link}

Why Gen Z in India Is Rewriting the Funding Playbook

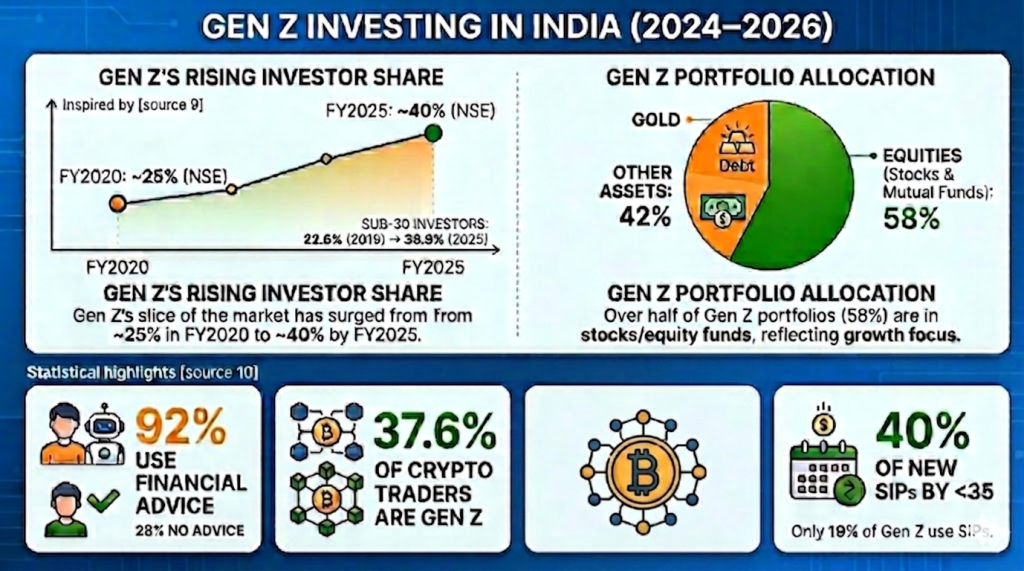

India’s Gen Z — these born between 1997 and 2012 — is essentially the most financially conscious younger cohort the nation has ever produced. Gen Z investing in India has been on an increase

In line with a report by NSE, over 56% of recent mutual funds SIP registrations in India now come from traders beneath the age of 30. For the monetary 12 months 2024-25 (FY25), the NSE noticed a 20.5% year-on-year improve in lively demat accounts, with a good portion of this development pushed by Gen Z and millennial traders

This isn’t unintended. Gen Z grew up with smartphones, survived the COVID-19 financial shock as youngsters, and watched their mother and father’ job safety erode in a single day. That have made them hungry — not only for cash, however for monetary independence.

However early enthusiasm and not using a technique is harmful. That’s why Gen Z investing in India must transcend Instagram reels and Reddit threads.

Gen Z Investing: What Makes This Era Completely different?

Earlier than diving into methods, it’s necessary to know what separates Gen Z traders from Millennials and older generations.

Digital-First by Default

Gen Z doesn’t go to financial institution branches. They open Zerodha accounts in 10 minutes, monitor SIPs on Groww, and uncover shares on Twitter (X) and YouTube. Their complete monetary life occurs on a 6-inch display.

Threat-Conscious however Not Threat-Averse

Opposite to what many assume, Gen Z in India isn’t afraid of threat — they’re afraid of uninformed threat.

Values-Pushed Investing

ESG (Environmental, Social, and Governance) investing is now not only a Western development. Indian Gen Z traders are more and more serious about inexperienced bonds, ESG mutual funds, and impression investing — aligning cash with private values.

Brief Consideration, Lengthy Imaginative and prescient

Paradoxically, Gen Z thinks in each 10-second reels AND 10-year targets. They need fast onboarding and real-time information, however many are already excited about FIRE (Monetary Independence, Retire Early) of their 20s.

Prime Funding Choices for Gen Z in India (2026)

Listed here are essentially the most viable and in style funding devices obtainable to Gen Z traders in India, ranked by accessibility and development potential.

1. Mutual Funds through SIP (Systematic Funding Plan)

Probably the most beginner-friendly possibility. Begin with as little as ₹100/month on platforms like Groww, Zerodha Coin, or Paytm Cash.

- Greatest for: Disciplined, long-term wealth creation

- Threat stage: Low to Excessive (relies on fund kind)

- Anticipated return: 10–15% CAGR (fairness funds, long run)

- Beneficial fund classes: Flexi-cap, ELSS (tax-saving), Index funds

2. Direct Fairness (Shares)

Shopping for particular person firm shares on NSE/BSE. Excessive reward, excessive threat — appropriate for Gen Z who’re prepared to analysis.

- Greatest for: These with time to trace markets

- Platforms: Zerodha, Upstox, Angel One

- Threat stage: Excessive

- Professional tip: Begin with blue-chip firms like Reliance Industries, Infosys, HDFC Financial institution earlier than exploring mid/small caps

3.Index Funds & ETFs

Observe market indices like Nifty 50 or Sensex. Decrease price than lively funds. Warren Buffett’s really helpful method for many retail traders.

- Expense ratio: 0.05%–0.20% (extraordinarily low)

- Greatest for: Passive traders who don’t wish to choose shares

- Common choices: Nifty 50 Index Fund, Nifty Subsequent 50, Gold ETFs

4. Public Provident Fund (PPF)

A government-backed financial savings scheme with tax-free returns. Boring? Sure. However highly effective for tax optimization.

- Rate of interest: 7.1% p.a. (tax-free)

- Lock-in: 15 years

- Greatest for: The danger-free portion of a Gen Z portfolio

5. Digital Gold & Sovereign Gold Bonds (SGBs)

Gold has historically been India’s favourite asset. Gen Z is accessing it digitally.

- SGBs: Issued by RBI, provide 2.5% annual curiosity + gold value appreciation

- Digital Gold: Accessible on Paytm, PhonePe — purchase in fractions

- Greatest for: Diversification and inflation hedge

6. REITs (Actual Property Funding Trusts)

Can’t afford a flat in Mumbai? Purchase models of a REIT beginning at ₹200–₹350.

- Examples: Embassy Workplace Parks REIT, Mindspace Enterprise Parks REIT

- Returns: Quarterly dividends + NAV appreciation

- Greatest for: Publicity to actual property with out large capital

7. Cryptocurrency

Excessive volatility, regulatory uncertainty in India, however undeniably current in Gen Z portfolios.

- Regulatory standing: Taxed at 30% flat on features (as per India’s crypto tax framework, in pressure since 2022)

- Platforms: CoinDCX, WazirX, CoinSwitch

- Advice: Restrict to five–10% of portfolio most

Step-by-Step: How you can Begin Investing as a Gen Z Indian

Observe this actual sequence to begin your funding journey the appropriate means:

Step 1: Construct an Emergency Fund First Earlier than investing a single rupee, save 3–6 months of bills in a high-yield financial savings account or liquid fund. That is non-negotiable.

Step 2: Open a Demat + Buying and selling Account You want a Demat account to carry shares and mutual funds. Prime selections:

- Zerodha (finest for lively merchants, flat ₹20/commerce)

- Groww (finest for novices, zero brokerage on mutual funds)

- Upstox (aggressive pricing, clear UI)

Step 3: Full Your KYC India’s KYC course of is now totally digital. You’ll want:

- Aadhaar card

- PAN card

- Checking account particulars

- A selfie + signature

Step 4: Begin Small with a SIP Start with ₹500–₹1,000/month in a Nifty 50 Index Fund. Let compounding do its work.

Step 5: Educate Your self Constantly Observe credible sources: SEBI’s investor training portal, Freefincal, Zerodha Varsity, and The Monetary Pandaa.

Step 6: Overview Your Portfolio Each 6 Months Don’t obsessively verify day by day. Set a calendar reminder for a semi-annual portfolio assessment.

Step 7: Seek the advice of a Monetary Advisor as You Scale As soon as your investable belongings cross ₹5–10 lakh, usher in a certified monetary guide or an authorized monetary planner (CFP) to information your subsequent section of wealth constructing.

Monetary Planner vs Monetary Advisor vs Monetary Marketing consultant: What’s the Distinction?

Many Gen Z traders use these phrases interchangeably — however they imply very various things. Right here’s a transparent breakdown:

| Time period | What They Do | Registration Required? | Preferrred For |

| Monetary Planner | Creates complete life-stage monetary plans (targets, insurance coverage, tax) |

CFP certification most popular | Lengthy-term purpose planning |

| Monetary Advisor | Affords funding recommendation + portfolio administration | CFP or related certifications most popular | Energetic portfolio administration |

| Monetary Marketing consultant | Broad time period — advises on monetary merchandise/options | Varies by specialization | One-time selections, enterprise finance |

| Wealth Supervisor | Holistic service for HNIs — portfolio + property + tax | SEBI licensed | ₹50L+ investable belongings |

Key Rule: Charge-Solely vs Fee-Primarily based

- Charge-only advisors cost you straight (₹5,000–₹25,000/12 months).

- Fee-based advisors earn from product sellers.

For Gen Z simply beginning out, a fee-only licensed monetary planner (CFP) is essentially the most reliable possibility — they cost you straight and don’t have any incentive to push merchandise.

How you can Confirm a Monetary Advisor’s Credentials in India

Earlier than hiring any monetary advisor, all the time ask for his or her CFP certification quantity, skilled expertise, and shopper references. Test if they’re fee-only (paid by you) or commission-based (paid by product firms) — this distinction straight impacts the standard and objectivity of recommendation you obtain.

When Ought to Gen Z Rent a Monetary Advisor in India?

Not everybody wants a monetary advisor instantly. Listed here are clear indicators that it’s time to rent one:

Rent a Monetary Advisor When:

- Your annual earnings crosses ₹10 LPA and taxes are getting complicated

- You obtain a lump sum (inheritance, bonus, ESOP payout)

- You’re planning to purchase property or take a house mortgage

- You’re getting married and wish to mix funds

- Your investable corpus exceeds ₹10 lakh

- You’re beginning a enterprise and wish wealth safety methods

You Don’t Want an Advisor But If:

- You’re investing lower than ₹10,000/month and simply began

- Your portfolio is just index funds or easy SIPs

- You don’t have any complicated tax scenario

The candy spot for many Gen Z Indians: begin self-directed, rent an advisor by age 28–32 or when monetary complexity will increase — whichever comes first.

Widespread Gen Z Funding Errors to Keep away from

Even essentially the most financially conscious Gen Z traders fall into these traps:

Mistake 1: FOMO-Pushed Investing

Shopping for a inventory as a result of it’s trending on Twitter. That is hypothesis, not investing. Keep on with your thesis and time horizon.

Mistake 2:Ignoring Inflation

A financial savings account paying 4% when inflation is 6% means you’re shedding cash in actual phrases. Your investments should beat inflation persistently.

Mistake 3: No Asset Allocation Technique

Going all-in on equities at 22 is okay — however having zero fixed-income allocation means you’ll panic-sell on the first market crash.

Beneficial allocation for Gen Z (aggressive profile):

- Equities: 70–80%

- Debt/Fastened Earnings: 10–15%

- Gold/Various: 5–10%

- Emergency fund: separate

Mistake 4: Skipping Tax Planning

ELSS funds save ₹46,800/12 months in taxes beneath Part 80C beneath the previous tax regime. NPS provides one other ₹15,600 beneath Part 80CCD(1B). Not utilizing these is leaving cash on the desk.

Mistake 5: Over-Diversification

Proudly owning 15 mutual funds that every one monitor related indices = similar threat, larger price, no profit. 3–5 well-chosen funds are higher than 15 overlapping ones.

Mistake 6: Treating Crypto as a Core Funding

Crypto is speculative. It has no intrinsic money circulate, no regulatory security internet in India, and a 30% flat tax charge on features. Deal with it as a high-risk wager, not a retirement technique.

The Position of Compounding: Why Beginning at 22 Beats Beginning at 32

That is the one most necessary idea for Gen Z investing.

Situation A: Rohit begins investing ₹5,000/month at age 22, stops at 32 (10 years whole).

Situation B: Priya begins at 32 and invests ₹5,000/month till 60 (28 years whole).

Assuming 12% CAGR:

| Complete Invested | Portfolio at 60 | |

| Rohit (began at 22) | ₹6 lakh | ₹3.04 crore |

| Priya (began at 32) | ₹16.8 lakh | ₹1.76 crore |

Rohit invested much less cash and ended up with ₹1.28 crore extra. That’s the compounding premium for beginning early.

Abstract

Key Takeaways for Gen Z Investing in India:

- Gen Z is essentially the most lively younger investing cohort in Indian market historical past, pushed by digital entry and monetary consciousness

- Begin with an emergency fund → open a Demat account → start SIPs in index funds Greatest newbie devices: Nifty 50 Index Funds, ELSS for tax financial savings, PPF for risk-free development

- A monetary planner focuses on life-stage purpose planning; a monetary advisor manages your portfolio; a monetary guide advises on particular selections

- Rent a certified monetary advisor or licensed monetary planner (CFP) when your portfolio or earnings complexity will increase considerably

- The most important benefit Gen Z has is time — compounding rewards early starters disproportionately

- Keep away from FOMO buying and selling, over-diversification, crypto overexposure, and tax planning neglect

FAQ

1. What’s the finest funding for Gen Z in India with low threat?

For low-risk Gen Z traders in India, Public Provident Fund (PPF), Sovereign Gold Bonds (SGBs), and liquid mutual funds are the most effective choices. They provide secure, inflation-beating returns with authorities backing. A PPF account might be opened at any submit workplace or approved financial institution with as little as ₹500/12 months.

2. At what age ought to a Gen Z Indian begin investing?

The best age to begin investing in India is as quickly as you obtain your first earnings — even when it’s an internship stipend. Beginning at 21–22 vs 28–30 can imply a distinction of crores in remaining corpus resulting from compounding. The minimal age for a Demat account in India is eighteen.

3. How a lot ought to Gen Z make investments per thirty days in India?

A sensible rule of thumb is the 50-30-20 rule: 50% of earnings on wants, 30% on desires, 20% on financial savings/investments. Even ₹1,000–₹2,000/month in a SIP is a superb place to begin. As earnings grows, improve the SIP quantity proportionally.

4. Do I would like a monetary advisor ifI’m simply beginning out?

No — you don’t want a monetary advisor once you’re simply beginning small. Self-directed investing by way of index funds and SIPs is totally manageable. Take into account hiring a certified monetary advisor or licensed monetary planner (CFP) as soon as your investable corpus exceeds ₹10 lakh or your monetary scenario turns into complicated (tax, actual property, enterprise).

5.Is cryptocurrency funding for Gen Z in India?

Cryptocurrency is extremely speculative and taxed at 30% on features in India with no loss offset profit throughout belongings. It may be a small half (5–10%) of a Gen Z portfolio, however ought to by no means be handled as a major funding technique. The regulatory setting in India for crypto stays evolving and unsure.

6. What ought to I search for when selecting a monetary advisor in India?

Search for a monetary advisor who holds acknowledged certifications corresponding to CFP (Licensed Monetary Planner) or CFA (Chartered Monetary Analyst), has clear charge constructions (fee-only is most popular over commission-based), and has verifiable expertise with purchasers in an analogous monetary scenario as yours. At all times ask upfront how they’re compensated — that is the one most necessary query that reveals potential conflicts of curiosity.

7. What’s the distinction between a monetary planner and a monetary advisor in India?

A monetary planner creates a complete roadmap protecting insurance coverage, targets, tax, and property planning — usually licensed as a CFP (Licensed Monetary Planner). A monetary advisor particularly manages funding portfolios and supplies market-related steerage. Many professionals provide each providers, however the titles carry distinct competency necessities and areas of focus.

8. How do I select the most effective SIP for Gen Z in India?

For Gen Z, the most effective SIPs are usually: (1) Nifty 50 or Nifty Subsequent 50 Index Funds for passive publicity, (2) Flexi-cap or multi-cap funds for diversified lively administration, and (3) ELSS funds for tax-saving beneath Part 80C beneath the previous tax regime. At all times verify the fund’s 5-year CAGR, expense ratio (decrease is best), and AUM earlier than committing.