")

{kind=link}

Again in 2020, I purchased a 5-year deferred fastened annuity, often known as a Multi-12 months Assured Annuity (MYGA). A MYGA, in essence, is sort of a CD issued by an insurance coverage firm. The insurance coverage firm ensures a set fee for a set interval. I spoke about MYGAs in my April 2021 presentation, Mounted Earnings Alternate options in a Low-Yield Setting.

I purchased the 5-year MYGA as a result of it was paying considerably greater than a 5-year CD from a financial institution or credit score union at the moment. The MYGA paid 3% a yr. The perfect 5-year CD was paying 1.5%. This MYGA had reached its 5-year assure interval final month. I ended it and pulled the cash again to my Constancy account.

The insurance coverage firm saved all its guarantees. All the things labored precisely as marketed. The MYGA was illiquid, with a prohibitive penalty in the event you withdraw greater than 10% of the steadiness every year, however I knew that getting in. The insurance coverage firm was a little bit gradual in processing paperwork, however it was nothing in comparison with the gradual handbook processing at TreausryDirect, which might take from six weeks to 10 months.

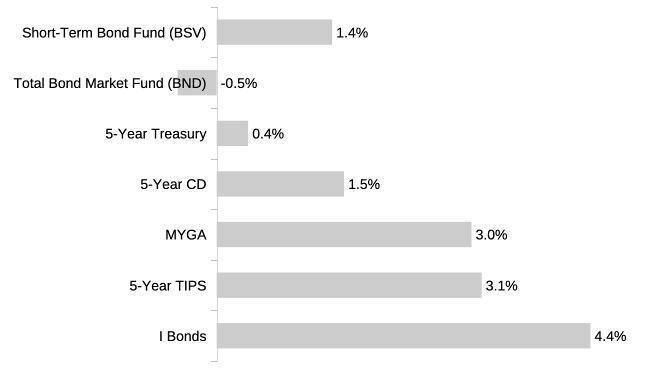

When it comes to funding returns, the MYGA did higher in these 5 years than a short-term bond fund, a complete bond market fund, a 5-year Treasury, and the very best 5-year CD. It trailed a 5-year TIPS by solely a hair. I Bonds did higher, however that they had low buy limits.

Nonetheless, I’d put my expertise with MYGA within the “profitable the battle however dropping the conflict” class. That’s why I’m not renewing it or shopping for one other MYGA.

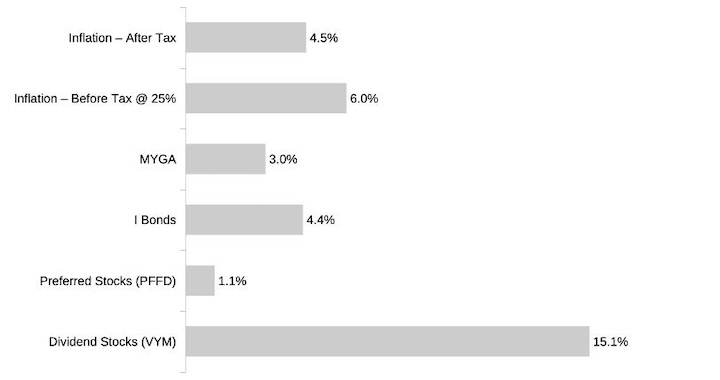

The conflict is towards inflation. Inflation averaged 4.5% a yr within the final 5 years. Since you pay taxes on the gross return, in case your tax fee is 25%, you’d should earn 6% a yr to maintain tempo with inflation. Seen by this lens, all bond investments misplaced to inflation within the final 5 years. The Vanguard Complete Bond Market Index Fund had a unfavourable 5-year return earlier than inflation.

Bond Substitutes

Burton Malkiel is the creator of the well-known ebook A Random Stroll Down Wall Road. He was making rounds within the podcast circle in the summertime of 2020 to advertise the twelfth version of that ebook. Mr. Malkiel referred to as the low-interest-rate setting at the moment “monetary repression.” He urged reducing the allocation to bonds and investing in most well-liked shares and high-dividend shares as “bond substitutes.”

Burton Malkiel’s suggestion for investing in “bond substitutes” was controversial at the moment. Some commentators went as far as to say it was silly. Now we see the outcomes after 5 years.

Most popular shares didn’t do nicely, however high-dividend shares did. Investing 50:50 in most well-liked shares and high-dividend shares outpaced inflation each earlier than tax and after tax. Bond substitutes received the conflict.

The Forest and The Bushes

My tour to MYGA reveals that we are likely to pay extra consideration to issues that may be analyzed with larger certainty, whereas neglecting issues which are extra unsure however have a extra important affect. I typically see folks asking questions alongside these strains:

Which cash market fund ought to I exploit?

Purchase I Bonds in April or Could?

Ought to I put money into Constancy’s S&P 500 fund (FXAIX) or Vanguard’s S&P 500 ETF (VOO). What about Constancy’s Zero fund?

TIPS ladder or TIPS fund?

Every query is sophisticated in its personal approach in the event you have a look at it underneath a microscope. There’s a strong spreadsheet that sends you an e-mail alert when it’s time to change from one cash market fund to a different. These choices make a distinction, however they simply fall into the “profitable the battle however dropping the conflict” class. Earlier than diving into the very best place to park your money, take into account whether or not you need to park that a lot money within the first place. Then you’ll keep away from a dilemma like this:

Saved up 1 million for a home we’re not shopping for, now investing it into the market

The large-picture choices don’t have a straightforward reply, however they make a a lot bigger distinction if you get them proper.

How a lot to put money into shares, bonds, money, actual property, Bitcoin, or gold?

U.S shares versus worldwide?

Worth shares or progress shares?

Developed worldwide international locations or rising markets?

Burton Malkiel received the “bond substitutes” proper. Nonetheless, his different options in the identical podcast episode for rising allocation to worldwide shares and rising allocation to rising market shares inside worldwide shares didn’t pan out. His arguments sounded convincing, and so they nonetheless do at this time, however the markets simply didn’t settle for them.

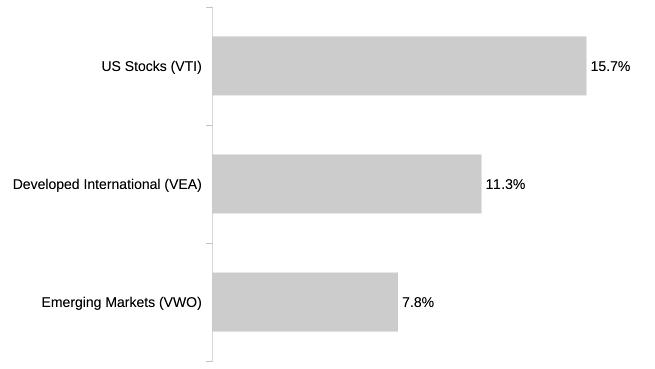

U.S. shares outperformed worldwide shares, and developed market shares outperformed rising market shares, each by a considerable margin. How a lot you invested in US shares versus worldwide shares, and in developed worldwide international locations versus rising markets, made an enormous distinction within the final 5 years. For this reason VTSAX-and-chill was a straightforward promote.

Possibly it should take extra time for these different options from Burton Malkiel to have the final snigger. Possibly they received’t ever catch up. Both approach, don’t lose sight of the forest if you look at the timber.

Be taught the Nuts and Bolts

I put all the things I exploit to handle my cash in a ebook. My Monetary Toolbox guides you to a transparent plan of action.